Biotech Trends to Watch: Reflecting on the First Half of 2024

If we talk about tech advances in pharma and biotech, the year 2024 has been a blast so far!

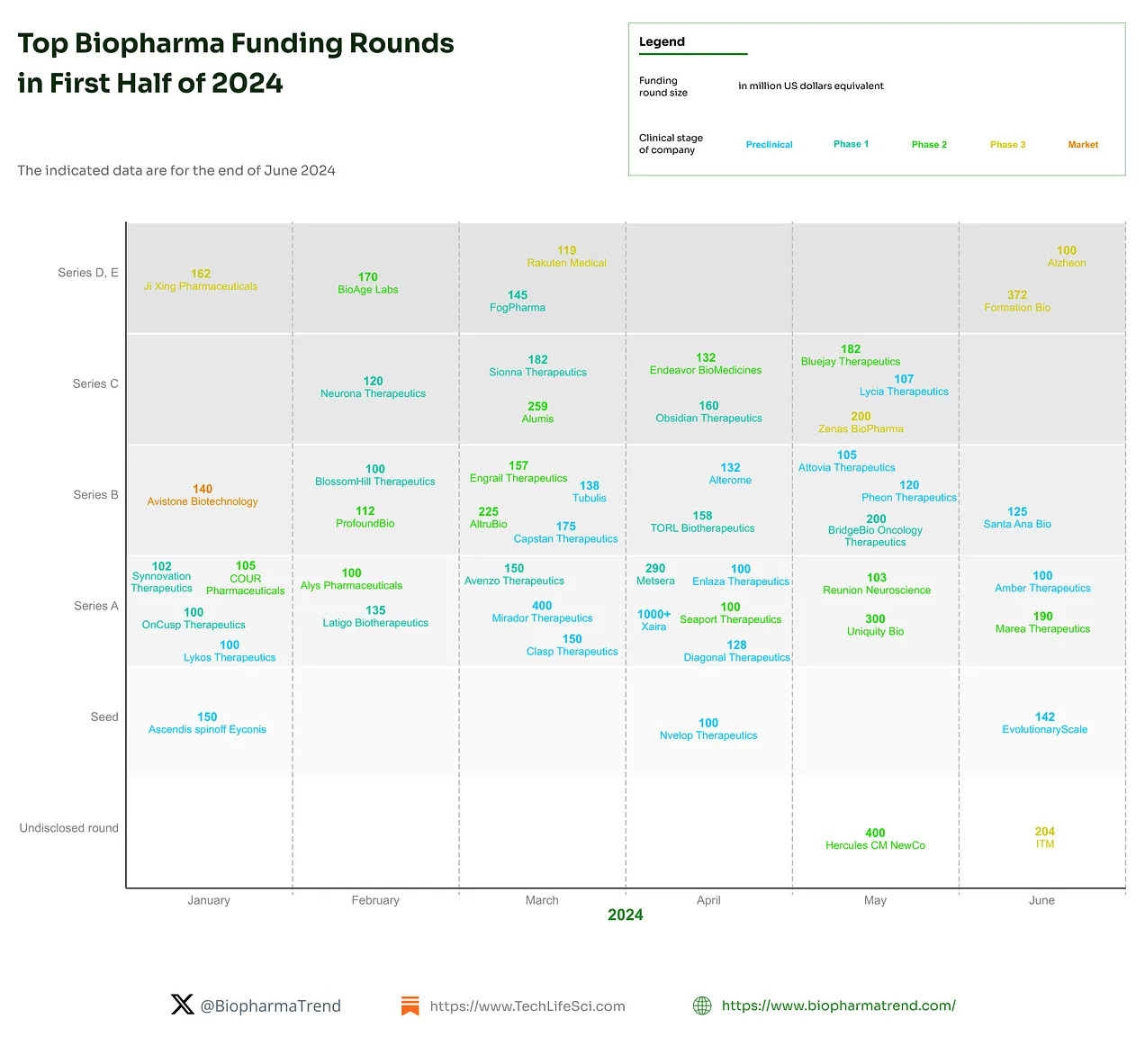

Last December I compiled a list of 11 Biopharma Trends to Watch in 2024 and I must say, the actual industry developments in all these areas in the first half of 2024 exceeded my expectations. Both in terms of scientific breakthroughs, and in business activity and financing dynamics (except stock markets which are weird in bio space, as usual).

Now, I’ve decided to review where we stand with some of the trends from my Christmas list half a year later, but today I am mostly focusing on the new trends that I picked to expand the list. So, it would still be relevant to check 11 Biopharma Trends to Watch in 2024 for the complete picture.

2024 is increasingly looking like a potential record breaker when it comes to VC dealmaking, with only the top 50 funding rounds approaching $9 billion (data from a table published by Endpoints News).

‘Organoid Intelligence’

In February 2023, scientists founded a new field: “organoid intelligence” (OI), which I consider one of the potentially most impactful ideas in the biological sciences—for the better or worse.

Led by Dr. Thomas Hartung in the U.S., they are developing biocomputers using brain organoids—lab-grown tissues mimicking organ functions—from human stem cells.

These brain organoids, though not structurally identical to human brains, exhibit neuron-like functions and are envisioned to surpass the computational efficiency of supercomputers, offering novel approaches to pharmaceutical testing and insights into brain functioning.

The field confronts technological challenges like scaling up organoids and developing brain-computer interfaces for data exchange. It also confronts ethical considerations regarding the potential consciousness and rights of these organoids, necessitating a rigorous and inclusive ethical framework for development.

This year we have seen progress by a Swiss biotech startup FinalSpark, which introduced the world's first bioprocessor using 16 human brain organoids.

The platform utilizes four Multi-Electrode Arrays (MEAs) housing the living tissue – 3D cell masses of brain tissue (organoids). Each MEA holds four organoids, interfaced by eight electrodes for both stimulation and recording. Data is transferred via digital analog converters (Intan RHS 32 controller) with a 30kHz sampling frequency and a 16-bit resolution.

The brain-computer interface on a chip technology uses in vitro cultured brain organoids coupled with electrode chips for information interaction through encoding, decoding, and stimulation-feedback, as described by Tianjin University’s Ming Dong. Although brain-powered robots are still a far-future concept, these organoids could help individuals with neurological conditions by potentially being grafted onto living brain tissue to stimulate neuron growth.

The term "Brainoware" was developed by Feng Guo, PhD, at Indiana University Bloomington, and Mingxia Gu, MD, PhD, at Cincinnati Children’s Hospital Medical Center.

It refers to brain-inspired computing hardware utilizing organoid neural networks (ONNs), which are self-organizing brain organoids connected to microelectrode arrays. These ONNs demonstrate unsupervised learning capabilities and hold promise for overcoming current AI hardware limitations, particularly in energy efficiency and processing complexity. The concept and findings were published in the article “Brain organoid reservoir computing for artificial intelligence” in Nature Electronics.

The successes in the field of organoid intelligence are closely dependant on the technological advances in the most vulnerable part of the tech stack: brain computer interfaces, the next item on our list of trends.

Brain Computer Interfaces

Continue reading

This content available exclusively for BPT Mebmers

We use cookies to personalise content and to analyse our traffic.

You consent to our cookies if you continue to use our website. Read more details in our

cookies policy.